Inflation, Employment, and Wages in the Current Recovery

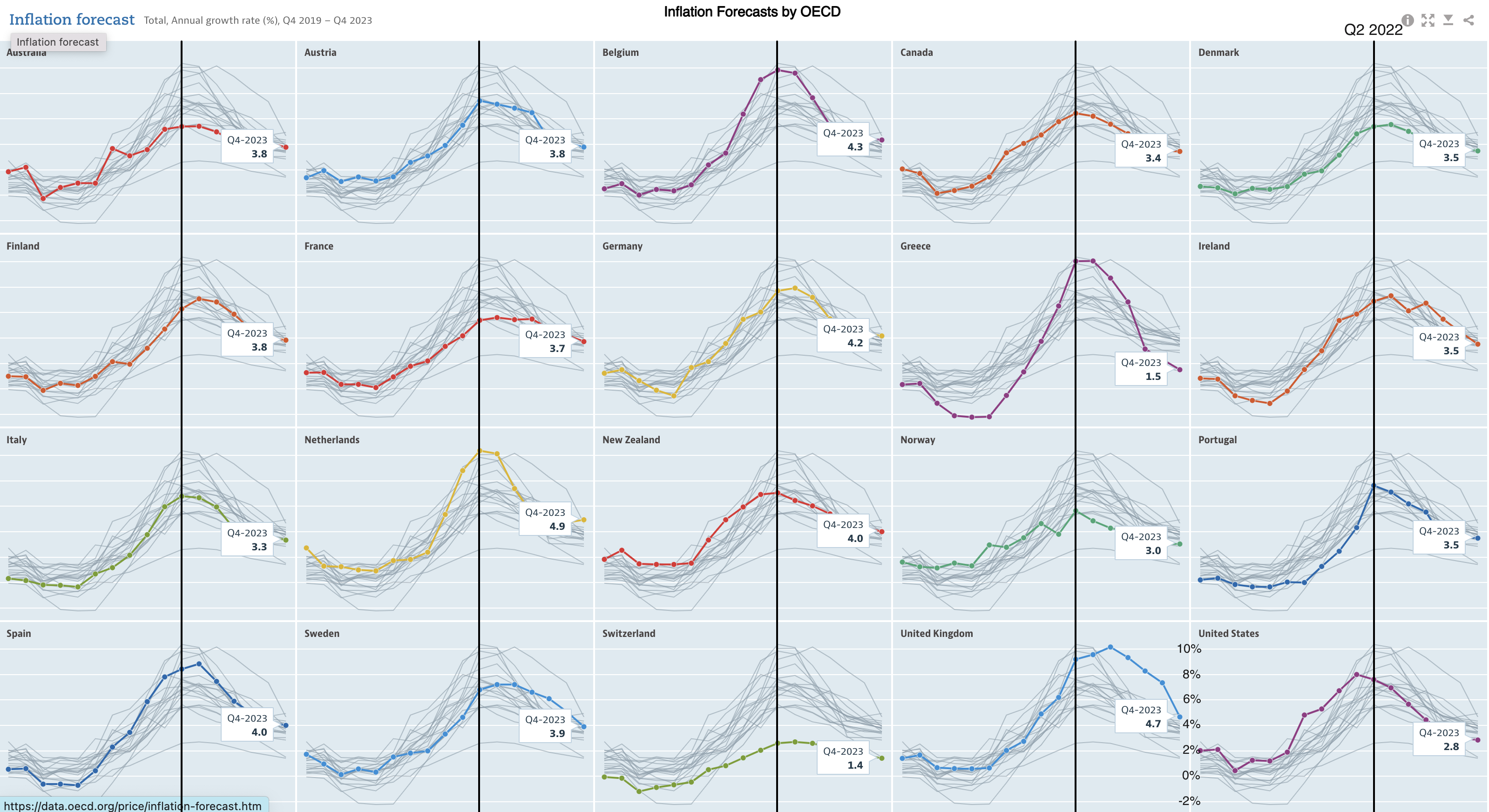

Inflation in the US Looks Similar

A simple point emerges from this summary of the experience with inflation in the leading European countries and the Anglo-offshoots: Across countries, the timing of the recent increase in inflation is very similar.

(Click the figure or here to download a larger version. I’ve added units on the graph for the US. The vertical black lines mark Q2 of 2022.)

I can’t claim to be an expert in the dynamics of inflation, but when I look at data like these, I see a common shock that started in 2021 as the world recovered from the Covid shock that was exacerbated by the war in Ukraine. In some countries, the amplitude of the wave was smaller (see e.g. Switzerland.) In others, the amplitude was larger (see e.g. the United Kingdom.)

If you poke around on the OECD website, it doesn’t take long to discover that the shock is concentrated in energy prices and food prices.

Unless you are willing to blame the war on policy makers in the US, it seems like a stretch to blame the inflation experience in the US exclusively on US economic policy.

One could argue that with different policies, the US would have had an inflation wave with a smaller amplitude – perhaps more like Switzerland than New Zealand. To make this case, one would also have to argue that an inflation wave with a smaller amplitude would be so valuable that it would justify the slower rate of recovery in the US labor market that it would surely have caused.

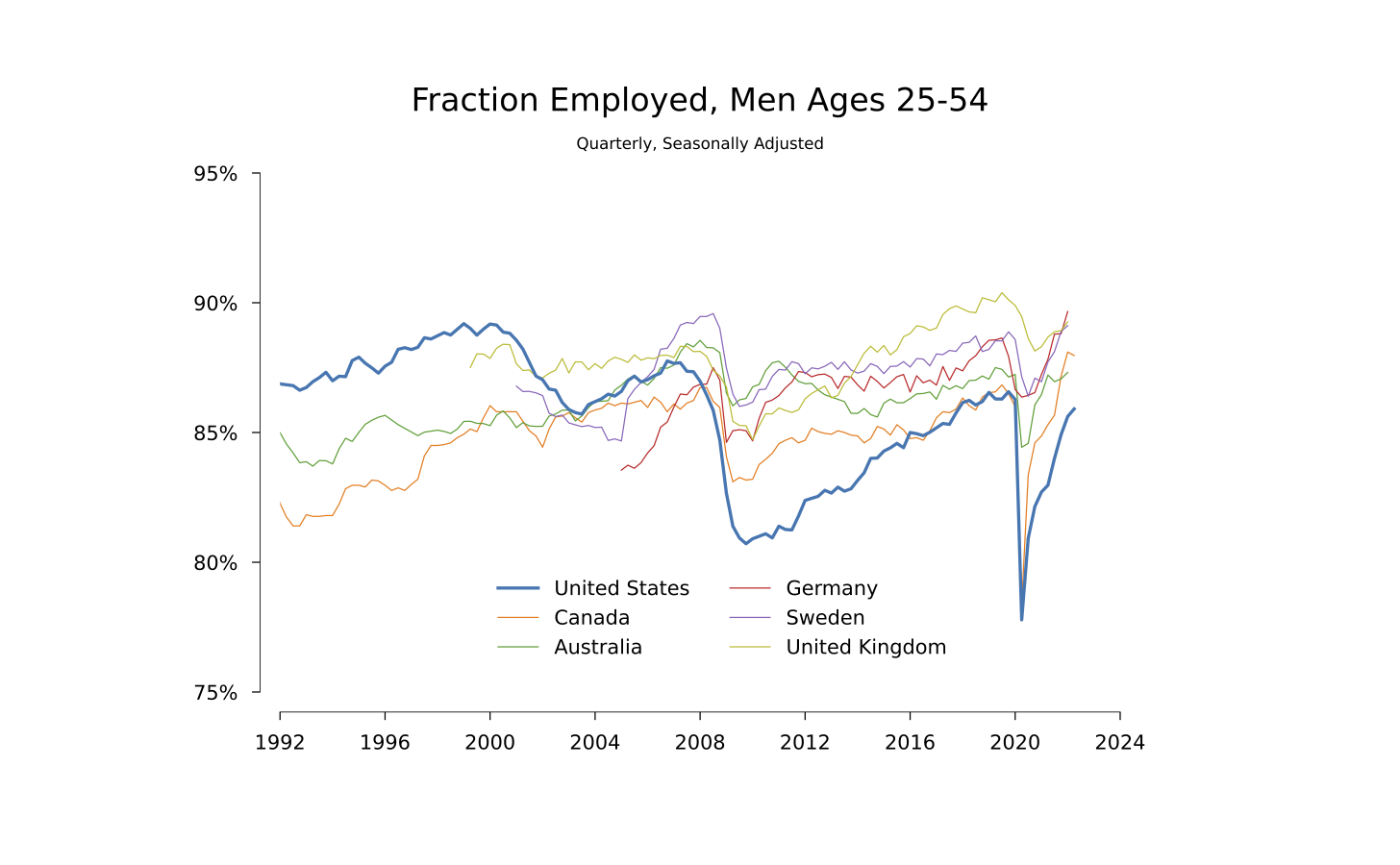

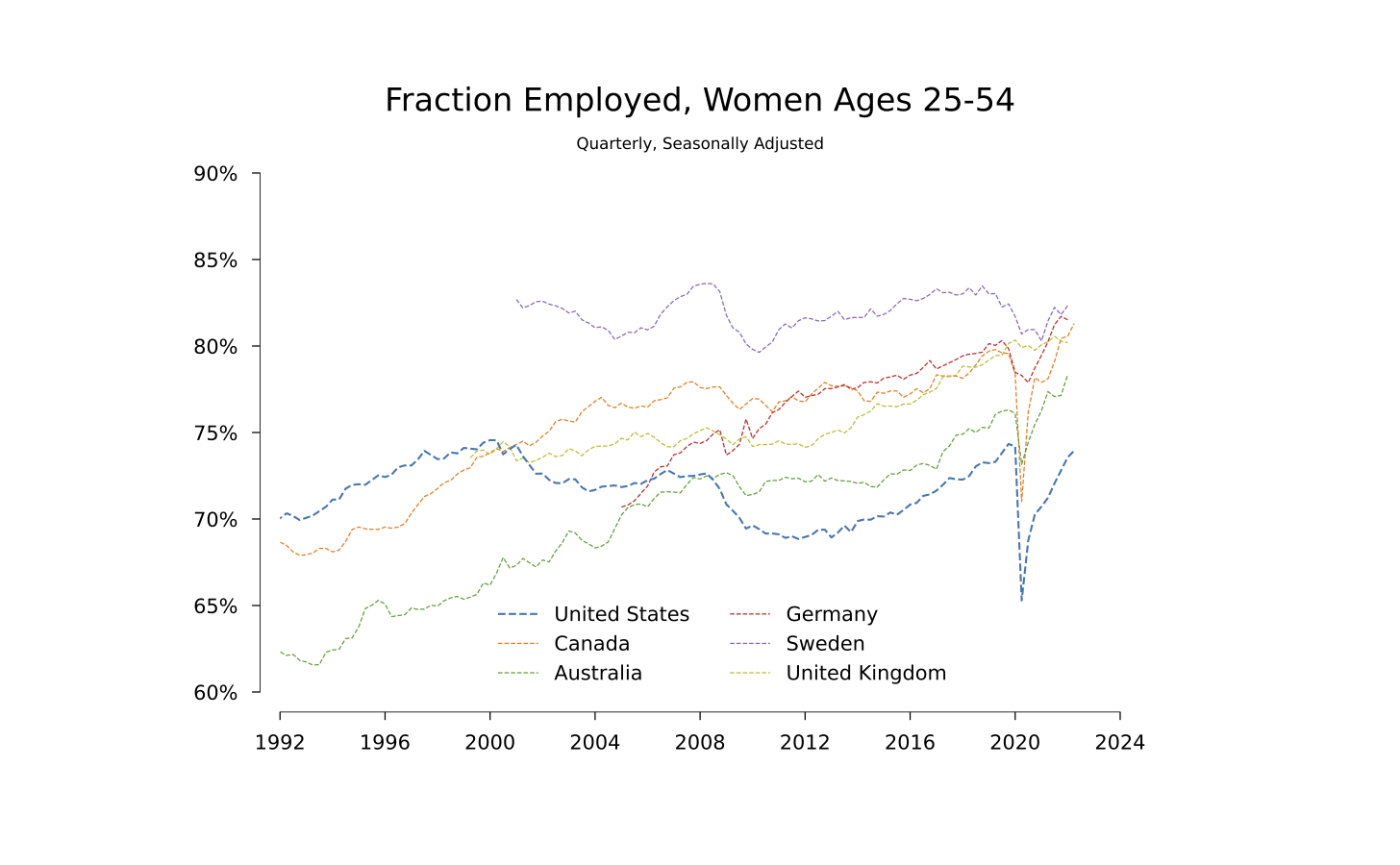

The Employment Rate Has Still Not Recovered

Given that the employment rate in the United States for both prime age men and women is still below its peak in 2019, and is falling ever farther behind the rates in other countries, it seems to me that it would be hard to make a convincing case that the US has been trying too hard to get people back to work.

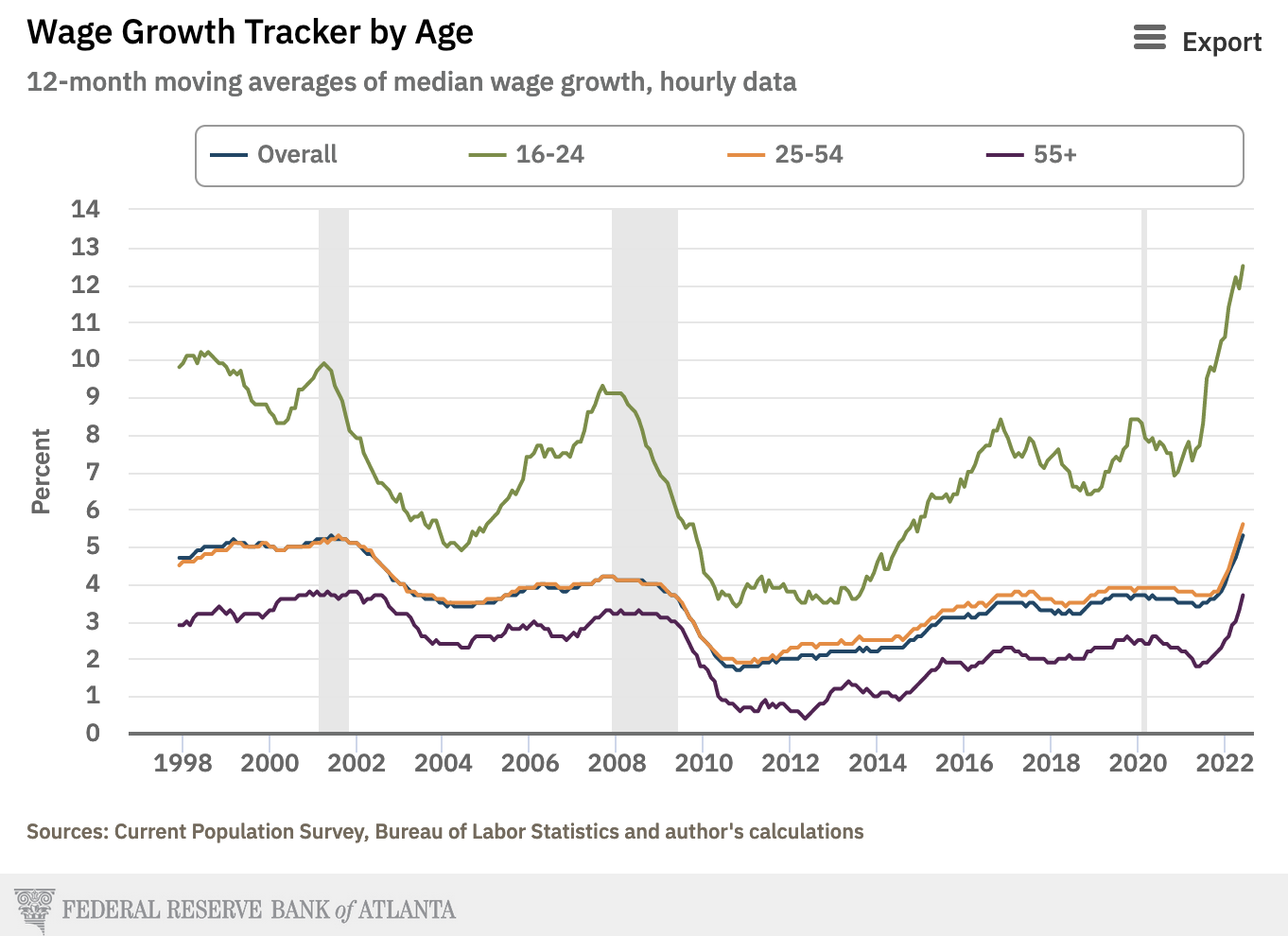

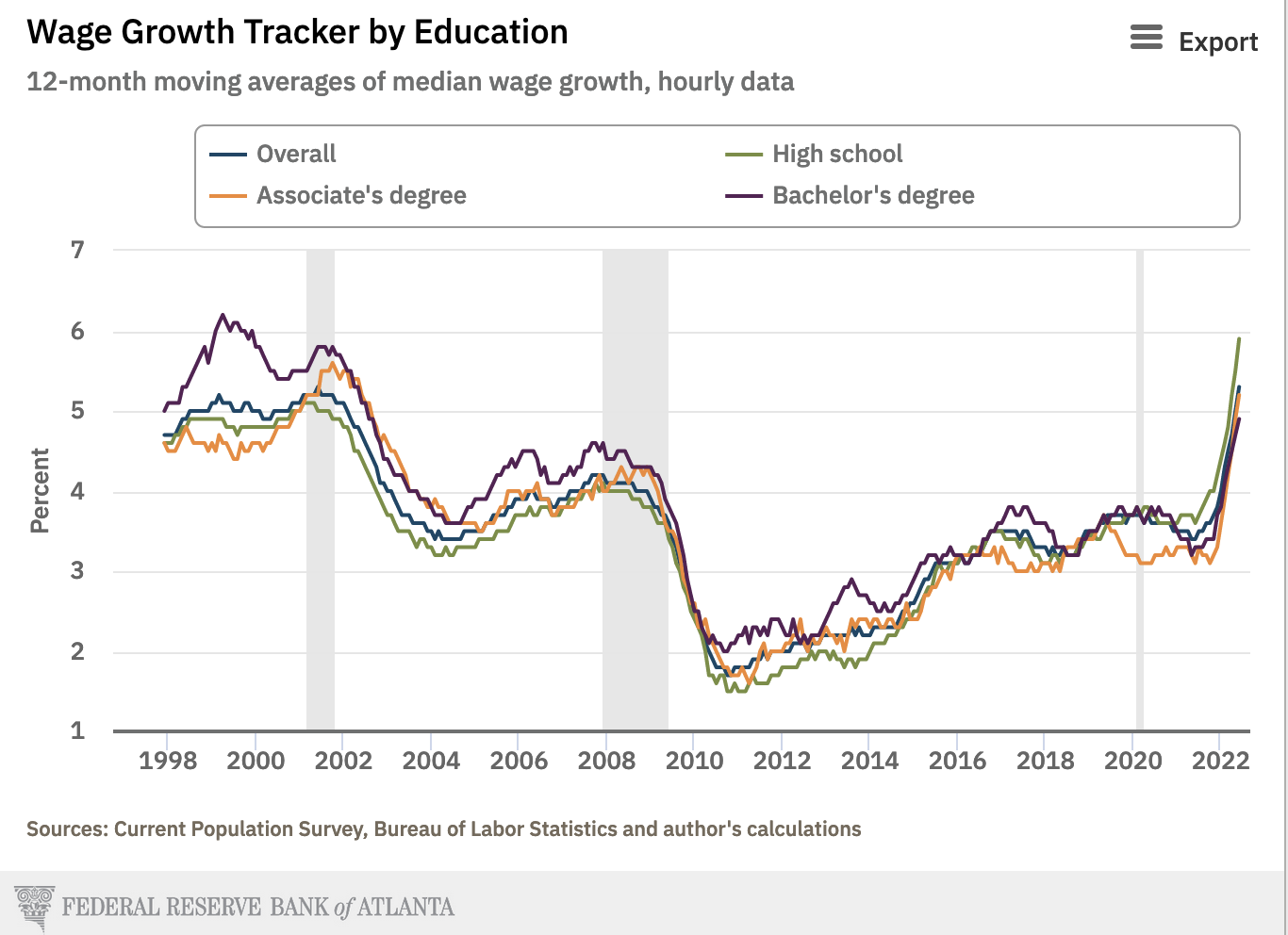

But Wages Are Increasing For Those Most Likely to Leave Work

The good news about the current expansion is that wages have been increasing especially rapidly for people with relatively low labor participation rates – young people:

and individuals with less education:

An increase in the relative wage for for those at the bottom of the wage distribution is welcome and long overdue. If it persists, there is reason to hope that it could help turn around the trend toward lower employment because work for many has been so unattractive.

Any serious discussion the benefits and costs of alternative policy should take account not just of its effects on inflation, but also on relative wages and the employment rate.