Inflation is About 2.8% and Still Falling

For the second year in a row, we’ve been through an entirely unnecessary spring quarter’s worth of hand-wringing about whether progress toward lower inflation has faltered.

This is a repeat of the mistake that I was boring on about last year. What’s the mistake? Why do “serious” people keep making it?

Signs of A Slowdown?

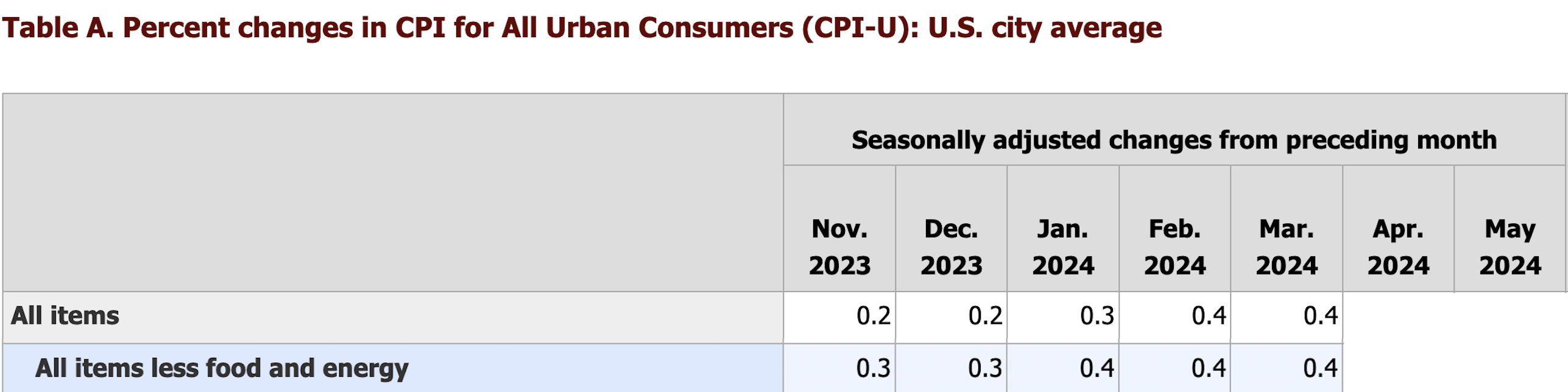

If you like numbers instead of graphs, here’s the table for you, from the CPI release from last week. I’ve removed some detail rows to focus on the so-called “headline” CPI and the CPI that ignores changes in food and energy. As I’ve been saying for more than a year, the headline measure is too volatile. The one that takes out food and energy is the best indicator of the underlying trend.

If you looked at these data as of March of this year, you might have been worried.

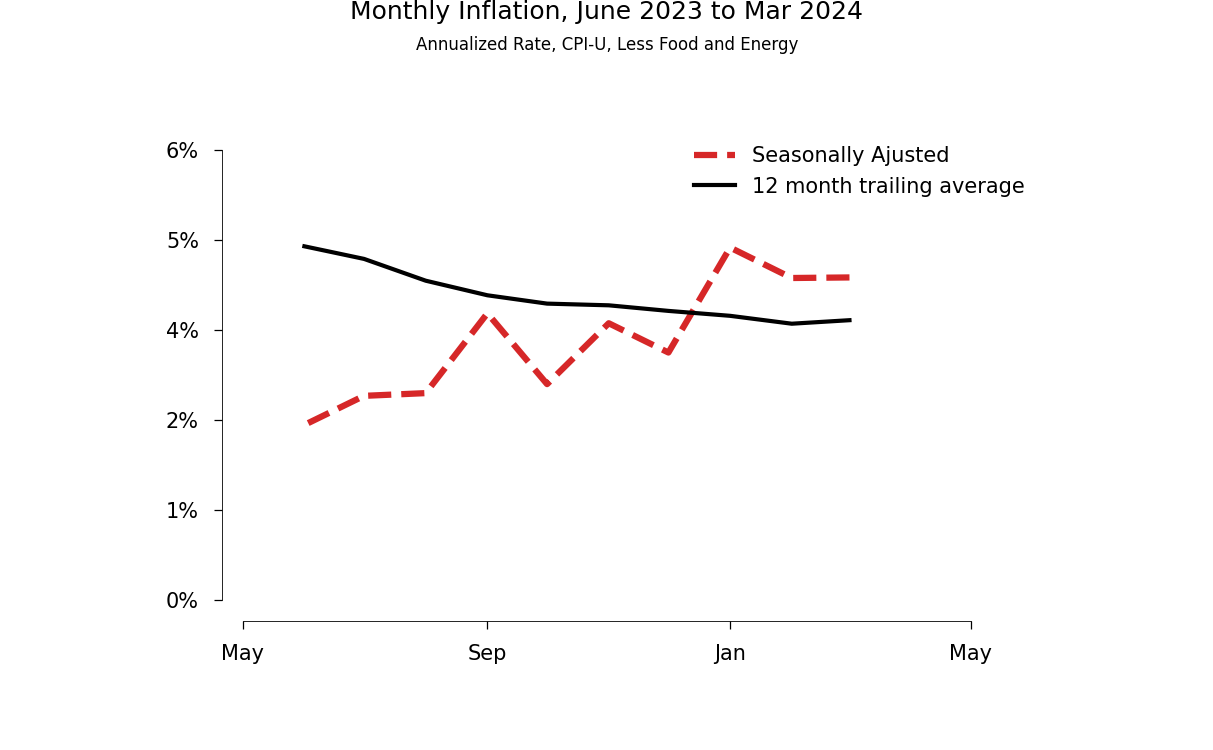

Back in March, things would have looked at least as bad if you had checked out a higher resolution graphical view of the same data. To make it easy to compare the numbers in the next graph to numbers that are familiar, I’ve annualized the rate of growth of prices in any month, which is a fancy way of saying multiply the raw percentage change by 12.

In this graph, you plainly see the same upward trend that was apparent in the table. I’ve also included the measure that the Fed likes to refer to: the 12-month average of the inflation rate.

The monthly data suggested that inflation was moving up. The 12-month average suggested that progress in bringing down inflation had come to a halt.

What a Difference Two Months Makes

Were these indications wrong? Absolutely.

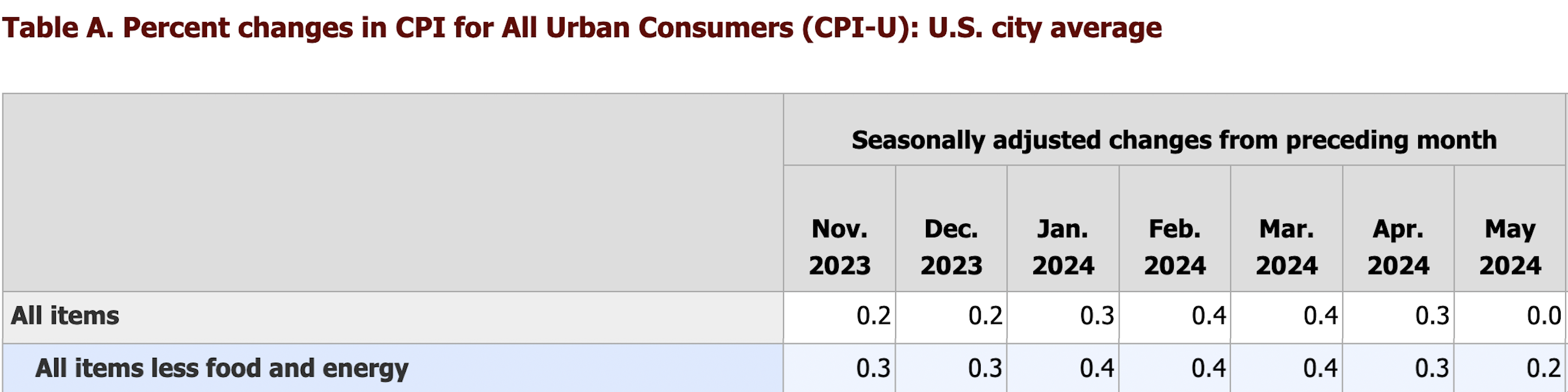

It is obvious that they were wrong about the trend. Look at the data from the table again, but this time, I won’t hide the values for Apr and May. (This table is from the BLS report that came out on June 12, 2024. Click to see the original.) As before, ignore the top line with the volatile headline measure of inflation and focus only on the line with data for the CPI minus food and energy:

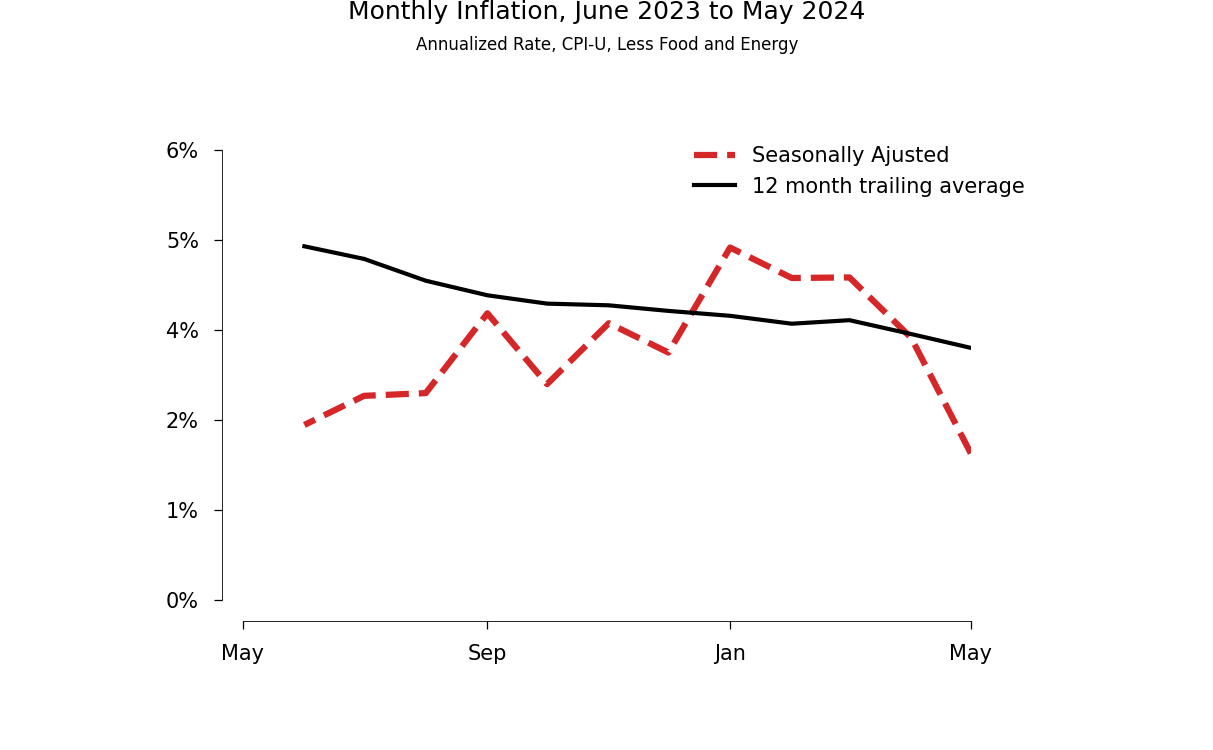

Now look at the updated graph.

The monthly rates are back down and the 12-month average is falling once again.

How Did I Know This Would Happen?

I knew that this would happen because each year tends to be like the year before, and we went through this last year.

But What Explains the Big Change in Two Months?

Seasonality.

For most of the last year, the monthly rate of inflation (measured on an annualized basis) was about 2%. But during Jan-Mar, it was about 6%. That’s a big seasonal effect.

But Why Doesn’t Seasonal Adjustment Fix This?

The statistical process for creating seasonally adjusted data always leaves some seasonality in the adjusted series. The right approach is to leave more when there is more uncertainty about the true seasonal effect.

In the current moment, we have very little data available for estimating the seasonal effect. The ideal conditions would be many years with the same macroeconomic conditions, including a constant trend rate of inflation. Because of the COVID shock and the global pattern of a rise, then fall, of inflation caused by the start of war in Ukraine (and perhaps exacerbated by recovery from the COVID shock), we are far from those ideal conditions.

There is a lot of uncertainty about magnitude and pattern of the seasonal effect in price changes. This is why the seasonally adjusted data that the BLS uses during the course of one year can change so much when they update the estimates of the seasonals at the beginning of the following year (and the year after.) Yes, that’s right. The seasonally adjusted inflation rate for Sept. 2022 that was reported during 2022 is different from the seasonally adjusted rate for Sept. 2022 that was reported in 2023. Or in 2024.

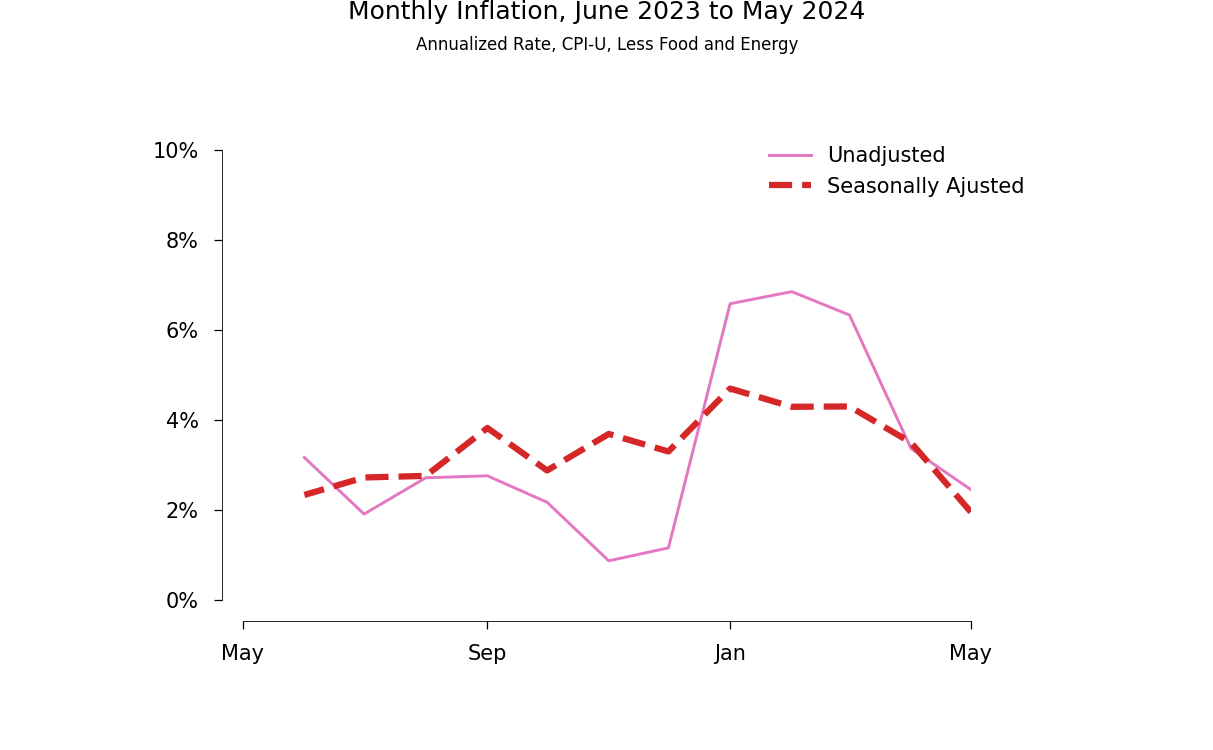

Right now, the seasonal variation that is left in the adjusted data for June 2023 to May 2024 is plainly evident in the next graph. The solid line is the raw monthly rate of change of prices. The thick broken line shows the same seasonally adjusted series that I displayed in the previous graph.

The raw data show that prices increase at a much faster pace during the first quarter of the year. The seasonally adjusted series is smoother than the raw series, but it still increases to an obvious peak in the first quarter of the year and decreases by about 200 basis points by the fall.

When I first saw how big the underlying seasonal was, and especially how big was the change in the BLS estimates of the seasonal at the beginning of 2022, I concluded that it is best to ignore the seasonally adjusted data and look for some other way to tell if the inflation rate was falling.

To be clear, this not a case where someone at the BLS is falling down on the job. There simply are not enough comparable, stable years to be able to estimate the seasonal with any precision. The BLS has to report its best estimate of seasonally adjusted data, but we do not have to use them to address the question that interests us—Is inflation still decreasing? There are other, better ways.

Same Month, Same Spot on the X Axis

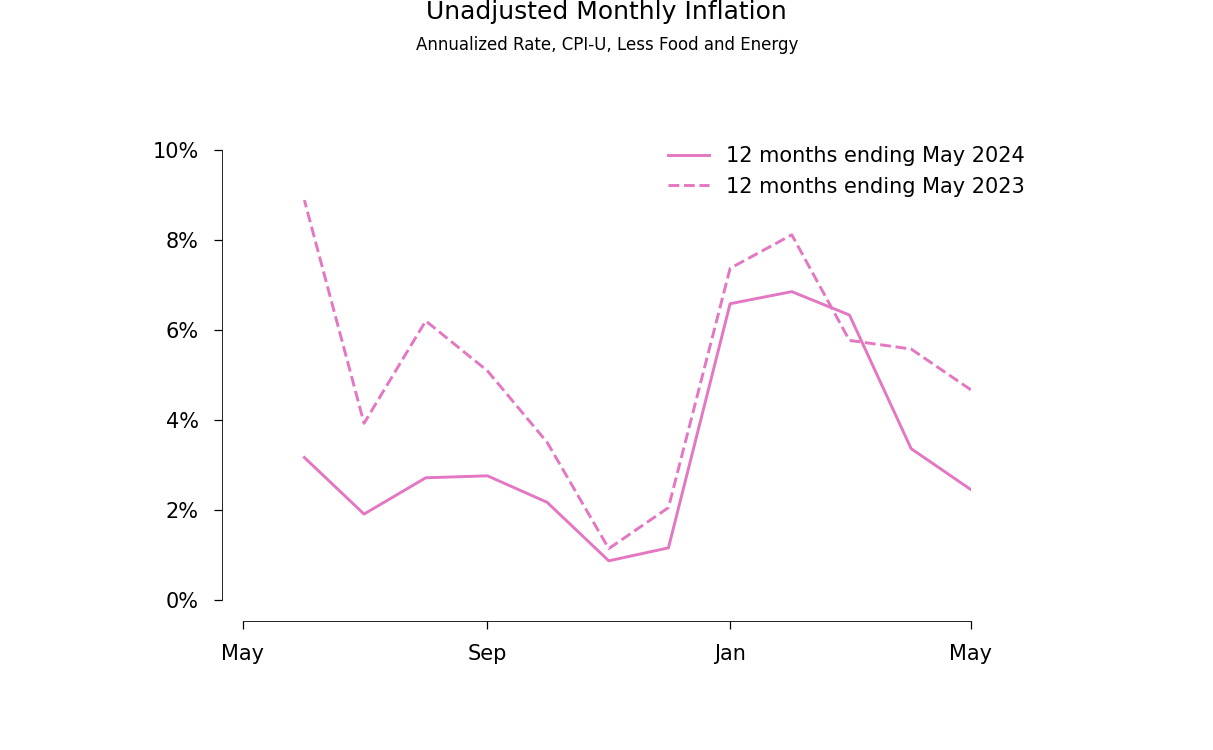

The next graph uses the unadjusted data to show that this seasonal pattern is evident both in the most recent 12 months and in the 12 months that came before. The main difference is that last year the background inflation rate was higher, particularly back in Mar of 2022.

This same month comparison also tells you the right way to check to see if the inflation rate is falling. From one month to the next, compare neither

-

seasonally unadjusted inflation rates, because these fluctuate with the season; nor

-

seasonally adjusted inflation rates because all the standard solutions to the signal extraction problem leave lots of signal in the noise when the uncertainty is high. So the seasonally adjust rates also fluctuate with the season.

The natural approach (and I have to say, the one I recommended repeatedly last year) is to compare inflation in the most recent January to inflation in the January from the year before; and to compare inflation in the most recent February to inflation in February of the year before; and so on, for each of the last 12 months. If the inflation rate in the most recent month tends to be lower than the inflation rate in the same month one year earlier, the trend inflation rate is coming down.

It is a trivial matter to see that that is the pattern we see in data over the last two years. In all but a single month of the last year, the inflation rate was lower than in the same month from one year earlier. (By the way, the odds that 12 flips of a fair coin will yield 11 heads are less than 1 in 100.)

If you’d rather see numbers than look at a graph, here you go:

The Change in the Monthly Inflation Rate

============================================================

(Precent Chg) minus (Percent Chg) = 12-month Delta

------------------------------------------------------------

Jun 2023 - Jun 2022 = -0.48%

Jul 2023 - Jul 2022 = -0.17%

Aug 2023 - Aug 2022 = -0.29%

Sep 2023 - Sep 2022 = -0.19%

Oct 2023 - Oct 2022 = -0.11%

Nov 2023 - Nov 2022 = -0.02%

Dec 2023 - Dec 2022 = -0.07%

Jan 2024 - Jan 2023 = -0.07%

Feb 2024 - Feb 2023 = -0.11%

Mar 2024 - Mar 2023 = 0.05%

Apr 2024 - Apr 2023 = -0.18%

May 2024 - May 2023 = -0.18%

Is the Inflation Rate 3.4%?

No. It is much lower.

If variable is falling and its average over a 12-month interval was equal to ||x||, at the beginning of the 12 months it was well above ||x|| and at the end it is well below ||x||.

This next table, with inflation over four 12-month intervals, is one final confirmation that inflation has been declining for the last two years.

======================================================

12 Month Interval Inf Rate Delta

------------------------------------------------------

Jun 2020 to May 2021 3.73%

Jun 2021 to May 2022 5.85% 2.12%

Jun 2022 to May 2023 5.19% -0.65%

Jun 2023 to May 2024 3.36% -1.83%

The inflation rate has clearly been falling. On average, the rate of change over the last 12 months was 3.4%. It follows that the inflation rate today has to be well below 3.4%.

Suppose that on average, over the last 12 months, the trend rate of inflation decreased by about 10 basis points each month. This would mean a reduction over the course of a year of 1.2%, which is substantially less than the actual reduction of 1.8% between the most recent 12-month interval and the previous 12-month interval. But to be fair, some of that reduction could have taken place before June 2023.

To be safe, let’s stick with an average monthly reduction of 10 basis points per month. For the measured rate of inflation over the last 12 months to hit 3.4%, the trend rate of inflation must have been roughly equal to 4.0% back in June 2023 and must now be close to 2.8%.